This article was originally published by Tyler Durden at ZeroHedge.

If you’re wondering why the Nasdaq is suddenly tumbling this morning, wonder no more…

Nasdaq moves lower after Meta announces it is to build a cloud business to sell its excess AI compute, weighing on cloud peers like AMZN, ORCL, MSFT and chip and memory names like NVDA, MU, INTO. As Bloomberg reports:

Meta, which has been rushing to secure expensive data centers and other infrastructure to fuel its own artificial intelligence ambitions, is forming a business to generate revenue from excess computing power sold to outside customers, according to people familiar with the matter, who asked not to be named as the details aren’t public.

One potential plan includes selling access to various AI models that are hosted on Meta’s existing AI infrastructure, an approach similar to AWS’s Bedrock offering, the people said.

Meta would run the data centers and chips that power the models, including its own Muse Spark models, and charge developers to access them.

The company is also considering selling access to “raw” computing capacity, akin to other so-called neocloud businesses like CoreWeave Inc., the people said.

…

Despite the complexities, Meta Chief Executive Officer Mark Zuckerberg has signaled to investors that he’s open to selling excess computing infrastructure, or even a so-called API service where customers would pay for AI usage — a business that’s usually measured in “tokens,” or the amount of data used and generated for a customer query.

“It’s definitely on the table,” Zuckerberg said during a call with shareholders in May.

“Almost every week there are different companies that come to us from the outside asking us to both stand up an API service or asking if we have compute that they could buy from us at some premium to what we’ve bought it at.”

This move comes after SpaceX started leasing its ‘excess compute’ (which is struggling now that it has competition in selling ‘compute’):

…raising questions about the potential for cutting CapEx which has perhaps overshot token demand…

…did META just shatter the market’s central premise has been that compute is scarce…

As Goldman Sachs 1-Delta desk-head, Rich Privorotsky, has been warning:

“The market’s central premise has been that compute is scarce. If scarcity persists, prices should remain firm and justify continued capex. If supply rises and rental prices continue to drift lower, that is a direct challenge to the shortage narrative. The first place that pain shows up is hardware.

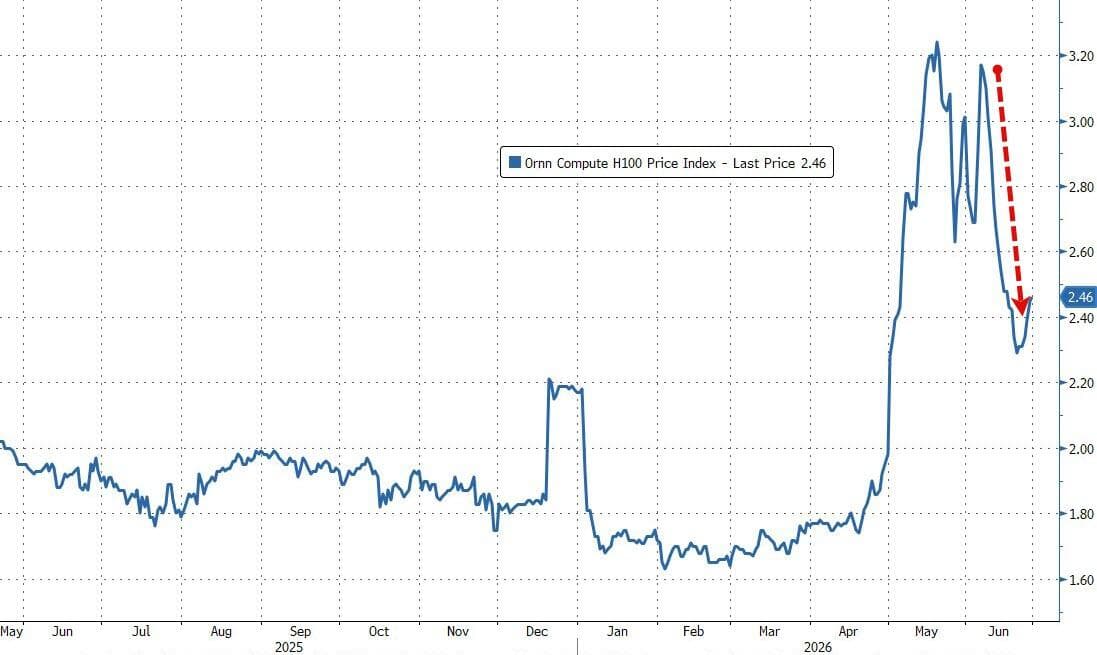

ORNN H100 index rolling over last couple days worth watching.

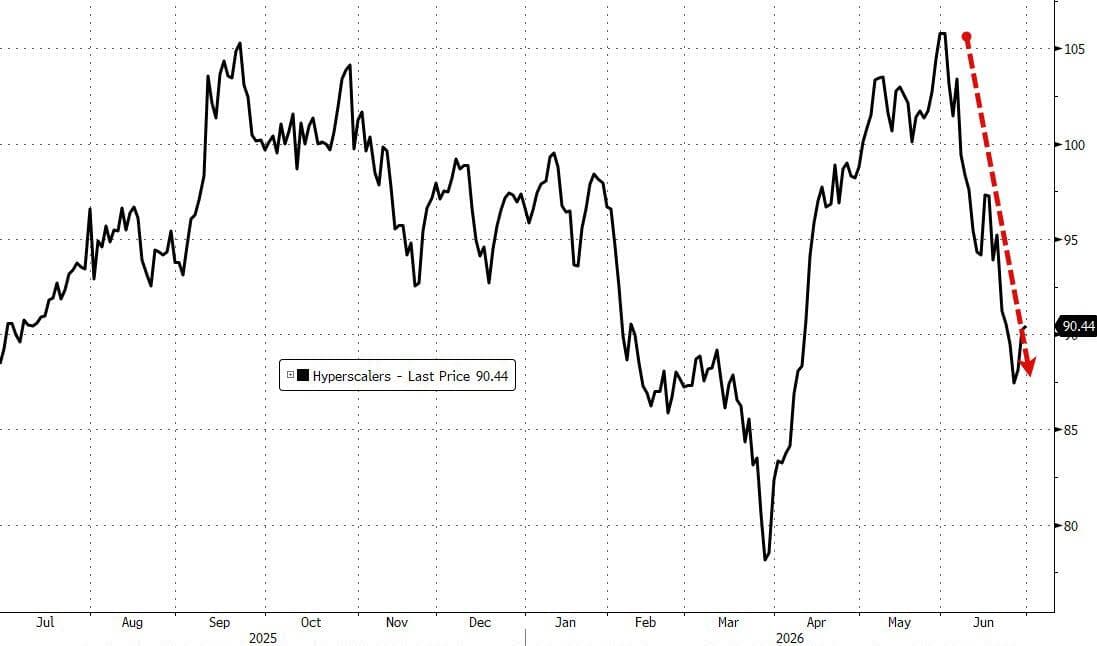

The beneficiaries are the companies selling the complete platform and monetizing usage rather than simply selling picks and shovels. My working conclusion remains that hyperscalers are the structural winners through this phase. The first moment they demonstrate they can deliver equivalent output with lower spend, the market will reward them.

The bigger risk sits further upstream in the hardware and infrastructure stack where expectations remain built around persistent scarcity.”

{kind=link}

Simply put, confessions of ‘excess capacity’ will crush the hyperbolic dreams of the CapEx cycle that underpins so much of the market’s recent incredible performance.

And the pivot to rewarding CapEx cutters begins…

“Lots of underperformance in hyperscalers. Everyone still appears convinced they must keep spending simply to remain competitive, while token cost compression/advent of neoclouds puts pricing pressure on core business. If token prices continue to compress alongside falling compute costs, the benefits may accrue to users faster than providers. Ironically, the first hyperscaler to signal that it can slow the pace of spending will likely see its share price rewarded.

If that happens, others will take notice.

That is the reflexivity that ultimately stalls the capex cycle… not a lack of demand, but investors deciding that incremental returns on the next dollar of spend are no longer attractive.

Watch hyperscalers share price as leading indicator.”

Don’t say you weren’t warned.

META shares are notably higher on the news…

Chipmakers are hurting…

_5.jpg)

The writing had been on the wall…

…and Premium Subscribers can read the full notes we have published over the past month here:

Buckle Up!

Read the full article here